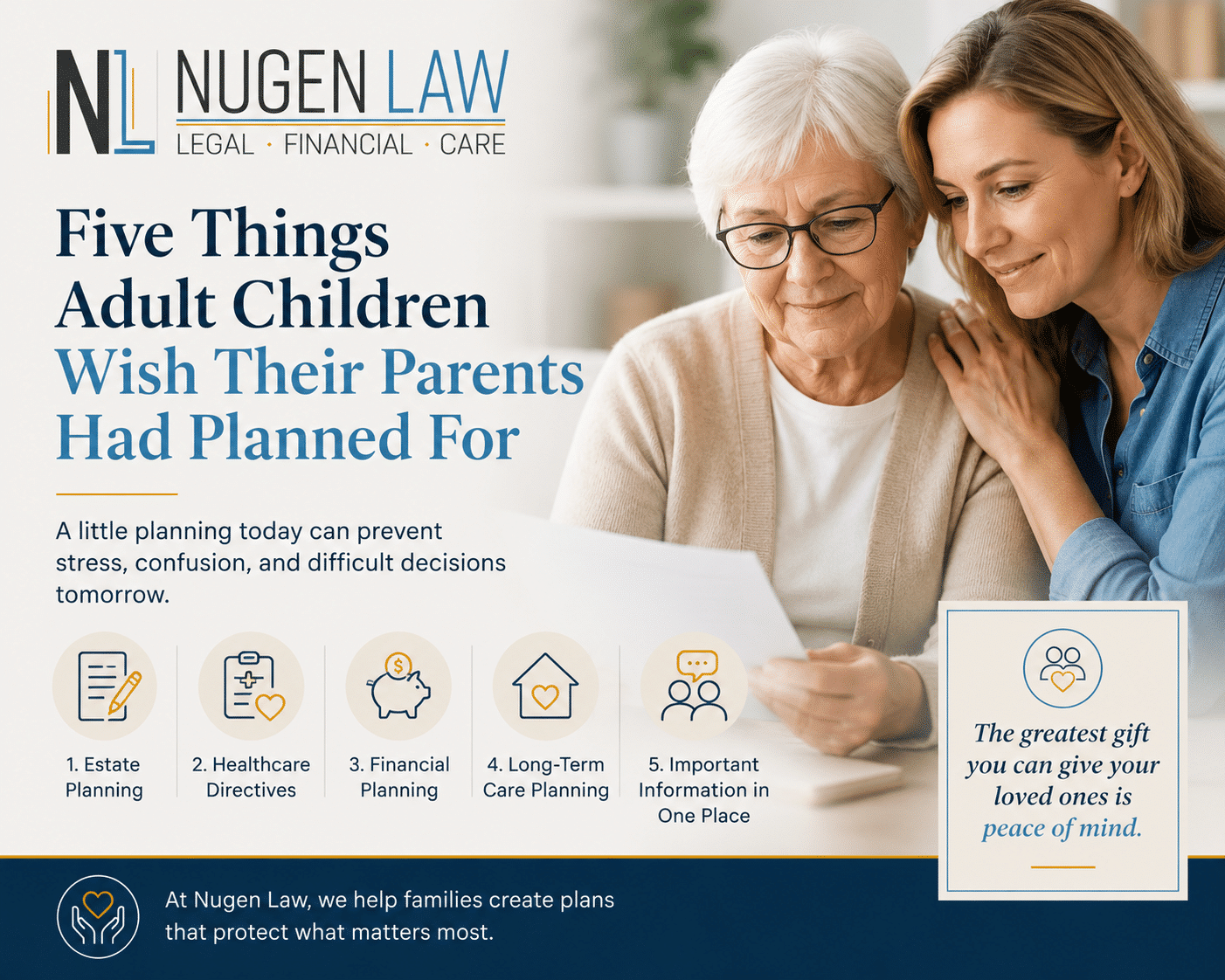

Have you ever heard an adult child say, “I wish we had talked about this…

The Medicaid Eligibility Process and Long-Term Care Planning

In 1965, Medicaid was established to provide healthcare to low-income and asset-poor individuals. The state and the federal governments cooperate in delivering benefits. The state you live in makes a big difference in determining when or if you are eligible.

Receiving other benefits such as Medicare, Social Security Disability Income, and Social Security Supplemental Income does not necessarily qualify you or disqualify you from being eligible for Medicaid. The state will look at these benefits and your income from working, rental properties, and dividends to determine if you meet the maximum income threshold.

In addition to states having a maximum income threshold, there is a maximum value of assets you can own and still be eligible for benefits. The government designed Medicaid as a last resort, meaning it expects you to spend most or all of your assets before receiving benefits.

Middle Class, Medicaid, and Long-Term Care

The biggest medical expense that many Americans will face is long-term care as they age. To avoid relying on Medicaid, many choose to purchase long-term care health care insurance, but that might not be the right answer for everyone, especially those already struggling to make ends meet. The monthly premiums are high.

Medicaid can be a lifesaver for those who need to go into a nursing home. Nursing home costs vary, but $10,000 per month is a reasonable estimate because they bill in an “all-inclusive” manner for food, lodging, and nursing care. A nursing home is an appropriate place for people needing extensive care but do not need to be in a hospital. For example, if a person can’t take care of their hygiene, feed themselves, take their medications, and notice when they are unwell, a nursing home is likely the best placement. Medicaid sometimes pays 100% of the cost of a nursing home.

People able to live more independently may choose different options, such as in-home care or a residential facility with less extensive care. Medicaid can still help with the medical portion of those expenses.

Leaving Property for your Heirs

Many seniors want to leave some property to their children, grandchildren, and other heirs, which is hard to do if you need to sell all your assets to pay for long-term care. The definition of an asset varies significantly from state to state. In many states, primary residences up to a certain value, where a person is still living, do not count as an asset that inhibits your ability to qualify for Medicaid.

It is important to know that you can’t reduce your countable assets by giving them away as gifts right before you need the care. For example, if you have 200k in stock, you can’t give it all away and then be eligible for Medicaid the next month. Medicaid uses a five-year “look back” period for gifting or transferring your assets. These laws and exceptions get quite detailed, and an estate lawyer or elder care lawyer can help you navigate their intricacies in your state.

To protect their assets for their heirs, many people choose to create an irrevocable trust. One type of irrevocable trust is called the Medicaid Asset Protection Trust (MAPT). MAPT is a great strategy for some people, but not all, to be able to leave property to heirs and still qualify for Medicaid benefits.

Three Reasons you Might Consider an MAPT

- You are confident you will no longer need access to the principal asset. After you transfer an asset to the MAPT, it will no longer belong to you or be in your control. But you may still be able to benefit from it. For example, you could put a rental property in a MAPT and use rental income, but you would not be able to sell the property and use the equity.

- You do not foresee needing Medicaid for five years or more. Remember that there is a look-back period for giving your assets away, which includes putting your assets in a trust.

- You have people that you can rely on for a long time with limited control over your assets. The trust is irrevocable, and they must follow the guidelines and act in your best interest.

Deciding on and Creating an MAPT

With the complexities of federal and state rules, you will want to consult a local attorney to help you decide whether a MAPT is the best choice. Take this opportunity to consider other legal plans like advance directives, wills, and living trusts to clearly define your wishes in the event of incapacitation or death. Your family members won’t need to guess your intentions or argue among themselves. Decision-making at emotional times will be kept to a minimum because they have already been made by you. We hope you found this article helpful. Contact our Auburn office at 260-925-3738 to create a plan that harmonizes its moving parts, so the gears will work together and you will leave the legacy you intended.

Related Posts