Have you ever thought that leaving assets directly to your adult children is the simplest…

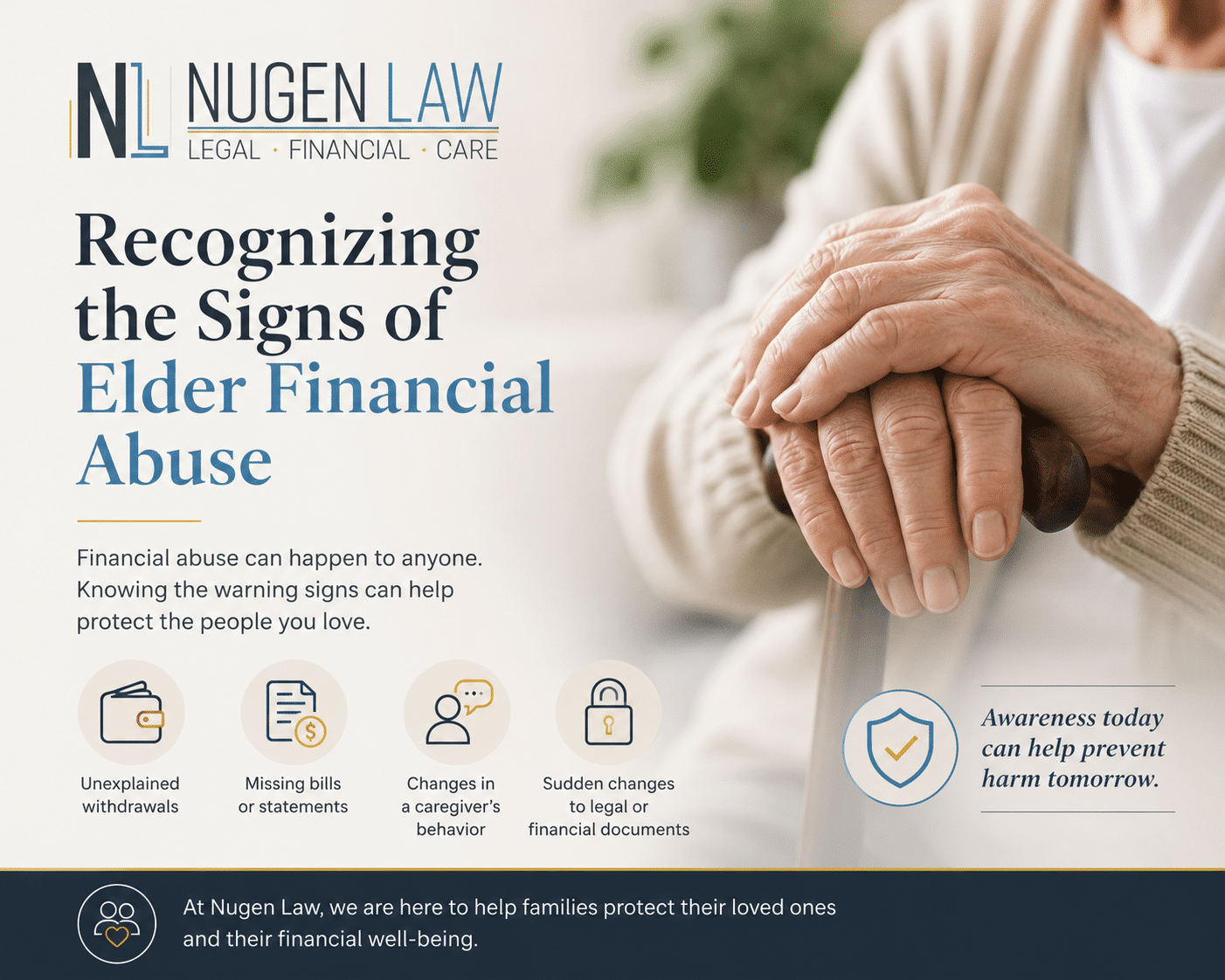

New Law Encourages Reporting of Elder Financial Abuse

Economic Growth, Regulatory Relief, and Consumer Protection Act

President Trump signed the Economic Growth, Regulatory Relief, and Consumer Protection Act into law on May 24, 2018. The Act contains a section that was once a stand-alone bill from Sen. Susan Collins (R-Maine) which is designed to encourage the reporting of elder (age 65 and older) financial abuse witnessed by financial institutions. The Act does not mandate that these institutions report financial abuse directed towards elders to avoid penalties, rather it gives them an incentive to do so. The Act provides immunity from any lawsuit alleging elder financial abuse if the financial institution reports it to state or federal law enforcement agents. To qualify for immunity, a financial institution has to create and administer a training program for employees to teach the employees how to spot elder financial abuse. This Act provides immunity to financial institutions because they are often the first to witness elderly clients making unusual transactions that may be linked to a scam.

The Act was inspired by the Senior$afe program in Maine. Senior$afe encourages state regulators, financial institutions, and legal organizations to work together on educating banking and credit union workers to spot and stop elder financial abuse. When elders have a trusted third party to talk to about their finances, they are less likely to fall victim to elder financial abuse, and this program has found success in reducing the amount of elders who fall victim to these scams.

However, this isn’t an entirely new idea. In 2016, the Consumer Financial Protection Bureau (CFPB) issued a report that found how reporting elder financial abuse has already become a respected norm in hundreds of counties around the country. The report found that these counties created voluntary community-based partnerships to prevent, detect, and respond to elder financial abuse situations. These partnerships often include entities such as financial institutions, adult protective services, and law enforcement. The CFPB found that these partnerships can be incredibly effective in protecting their elderly citizens. What’s more, in states without elder financial abuse protection laws, these community efforts have created a sense of responsibility within these counties to protect their most vulnerable from financial scams, without reward or threat of prosecution against financial institutions. Following this report, the CFPB released a resource guide and best practices to help and encourage other counties across the US to adopt their own protection partnerships. Among other recommendations, the CFPB encourages communities to directly include law enforcement and financial institutions in these partnerships. Financial institutions are often the first to spot these cases, and law enforcement has an obligation to investigate once a claim is made. Also, the CFPB recommends that partnerships which serve diverse areas engage with groups that are already entrenched in the community, such as service groups or faith-based organizations.

Protecting our most vulnerable is important to providing a safe and prosperous society for all citizens. These community-based partnerships and the Economic Growth, Regulatory Relief, and Consumer Protection Act are both steps in the right direction towards protecting those who aren’t able to protect themselves. If you have any questions about something you have read, please do not hesitate to contact our office.

Related Posts